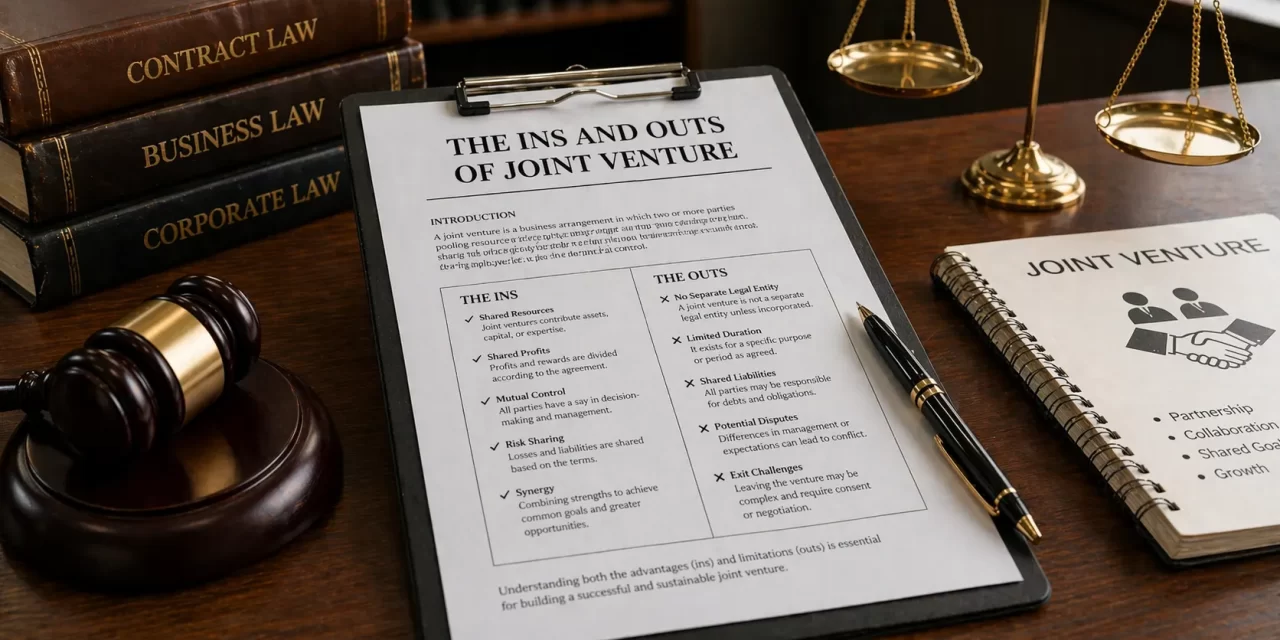

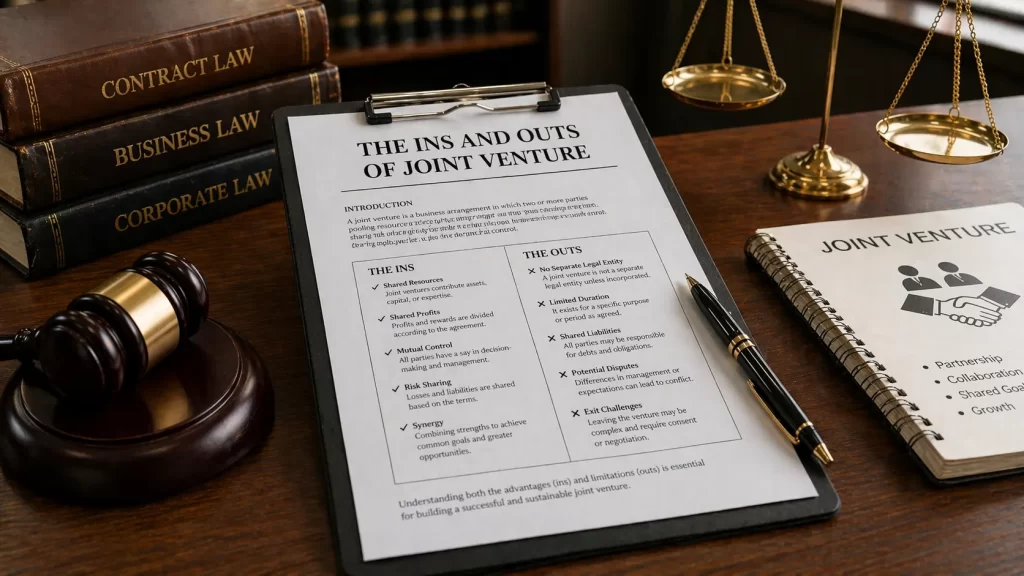

A joint venture (JV) is a business arrangement in which two or more parties pool their resources for the purpose of accomplishing a specific task, such as a new project or other business activity. In a JV, each participant is responsible for profits, losses and costs associated with it. However, the venture is its own entity, separate and apart from the participants’ other business interests.

JVs can be either incorporated or non-incorporated. If incorporated, the JV agreement will establish a new legal entity. If it is non-incorporated, it will be a business entity, financially and operationally separate from the parties to JV, but no legal entity is set up. These two forms, especially the non-incorporated JV, can take various forms.

Rules for incorporated JV refer to the limited liability company law in Indonesia. The benefits of this model are that the law is clear on issues such as distribution of profits, voting rights, dissolution, liquidation, and other aspects. Accordingly, the parties do not need to regulate specifically what has already been stipulated in the law, unless they want to make special arrangement.

Rules for non-incorporated JVs depend on the arrangement set out by the parties. The agreement will have many terms, since almost all aspects similar to a company must be regulated. This model offers more flexibility in which provisions to adopt from the company law, and which special provisions.

The flexibility in a non-incorporated JV is the weakness in the incorporated JV. There are some fundamental terms from which the parties cannot deviate. Even though this creates legal certainty, the commercial arrangement may not be stipulated differently for what is expected under the law. On a contrary, in a non-incorporated JV, the parties may feel uncertainty since everything is only regulated by the agreement. Despite pacta sunt servanda (an agreement must be kept) principle, there may be a challenge in implementing or interpreting some of the agreement’s provisions.

If a JV involves an asset such as real property, an incorporated JV can legally own it. In contrast, a non-incorporated JV cannot legally own real property. Therefore, it has to be held by one of the parties in the JV. A claim by a third party, such as a creditor, can result in an execution of its assets, bankruptcy proceedings, or postponement of debt payments obligation. These actions can impact the JV’s other partner, especially if the asset is significant to the non-incorporated JV. From this perspective, if it involves real property, an incorporated JV seems a better model than a non-incorporated JV, and if no real property, a non-incorporated JV may be preferable.

Management guru Peter Drucker once said businesses grew by one of two ways: grassroots up, or by acquisition. Today businesses can grow through alliances. On the contrary, some JVs may hurt the other partner. Hence, as a JV may be hard to understand, professional advice for them is imperative. The intent is, at least, to legally protect JV participants from business and legal risks of the JV. Lastly, tax advice is important so that JV participants can appropriately allocate their resources.

*This column has been published in Forbes Indonesia magazine and http://forbesindonesia.com/berita-1401-the-ins-and-outs-of-joint-ventures.html